Personal Finance Essentials as a Pharmacy Student

No matter your background or student loan amount, there are a few fundamental personal-finance principles that all students and professionals should be aware of, and possessing the right mindset is key to ensure long-term financial well-being.

Introduction

According to the recent 2023 American Association of Colleges of Pharmacy (AACP) Graduating Student Survey, the median amount of money borrowed to finance a PharmD education was $158,000,1 and students continue to feel the burden of student loans while balancing their studies, internships, committees, investments, and post-graduation opportunities. No matter your background or student loan amount, there are a few fundamental personal-finance principles that all students and professionals should be aware of, and possessing the right mindset is key to ensure long-term financial well-being.

Personal finance is simply managing your money, including saving and investing. Within the umbrella of personal finance includes budgeting, insurance, debt, retirement, tax, and estate planning2. Personal finance is truly “personal” and what may work for one individual may not translate well for another individual. However, understanding the key basics of personal finance will alleviate many of the common stressors students and pharmacists face when formulating a plan.

Budgeting

The first key principle to understand is the importance of and sticking to a budget. A budget is a plan for your money. There are a variety of approaches to budgeting, such as zero-based budgeting, 50/30/20, the envelope system, pay yourself first, etc. Additionally, there are a variety of tools to assist in your budgeting process: You Need a Budget (YNAB) and EveryDollar for zero-based budgeting, Goodbudget for hands-on envelope budgeting, Empower Personal Wealth for tracking wealth and spending, PocketGuard for a simplified budgeting snapshot, Honeydue for budgeting with a partner, and more.3 For those who are more Do-It-Yourself, tracking savings and spending with Google Sheets or Microsoft Excel are simple options to truly take ownership over budgeting principles. The important concept to remember is that there’s no one perfect approach or method. In fact, the best method is the one that you will adhere to over the long-term. Experimenting with a variety of methods and tools will help narrow down which approach is best for you while fitting into your lifestyle. After sticking to your budget, it’s paramount to live on less than you make and save/invest the rest.

- Zero-based budgeting:

- Every dollar has an assignment

- Take your monthly income and use every dollar in a deliberate way (savings, utilities, groceries, investments, debt payments, etc.)

- Stop when there are zero dollars left

- 50/30/20:

- 50% of income on needs

- 30% of income on wants

- 20% of income on savings/debt paydown beyond minimums

- Envelope System:

- Set a spending limit for each expense category

- Fill envelopes with the allotted cash you can spend in each

- Once envelope is empty, you can’t spend any more money on that category for the month

- Pay Yourself First:

- “Reverse” budget that puts savings before immediate expenses

- Decide how much to set aside for savings goals first

- Use the rest for bills and other costs

Emergency Fund

After taking control over your spending and savings, most financial advisors will suggest opening and saving within an Emergency Fund. An emergency fund, otherwise known as a rainy day fund, is a set of money reserved, typically in a high-yield savings account, that one doesn’t touch unless he or she truly needs it for an emergency. That way, you’ll be ready for whatever comes your way and not consider selling certain investments or taking on more debt just in case. A typical starting amount to fund in an emergency fund is $1,000, but many advisors consider savings ideally 3-6 months of living expenses.

Debt & Student Loans

Safe practice is to always borrow the least amount possible to fund education and living costs. Additionally, you can always apply for more aid during the year if needed. However, given the rising costs of tuition and living expenses, it’s no wonder why the student loan burden continues to increase year over year. There are a variety of viewpoints when it comes to debt, but it’s important to consider the difference between assets and liabilities. In short, an asset is simply anything you own that adds to your overall value, and a liability is anything that you owe to others. Although pharmacy school is an investment in one’s education, student loans are a liability, since you owe money to a servicer to fund education. With that being said, there are a variety of approaches to paying off debt and managing student loans. The two most common approaches are the debt snowball method and the avalanche method. The debt snowball method involves:

- Listing all debts from smallest to largest

- Making the minimum payments on all your debts except the smallest debt

- Throwing as much extra money as you can on your smallest debt until it’s gone

- Taking what you were paying on your smallest debt and adding that to your payment on the next-smallest debt and repeating

The avalanche method, however, involves a similar approach but tackling the debt with the highest interest rate first then working down to the debt with the lowest interest rate. Below are a list of a few tips, tricks, scholarships, and programs to minimize the student debt burden:

- Consider internships or side job options to help offset cost

- Pay of interest on loans while in school

- Military programs

- Navy Health Services Collegiate Program (HSCP)

- Air Force Health Professions Scholarship Program

- Army Armed Forces Active Duty Health Professions Loan Repayment Program (ADHPLRP)

- Indian Health Service (IHS) Scholarship

- Native Hawaiian Health Scholarship

- American Society of Health-System Pharmacy (ASHP) Student Leadership Award

- J.C. and Rheba Cobb Memorial Scholarship (NCPA Foundation)

- Neil Pruitt Sr. Memorial Scholarship in Entrepreneurship (NCPA Foundation)

- Tylenol Future Care Scholarship Award

- Express Scripts Scholars Program

- Local school/state-specific scholarships

Investments

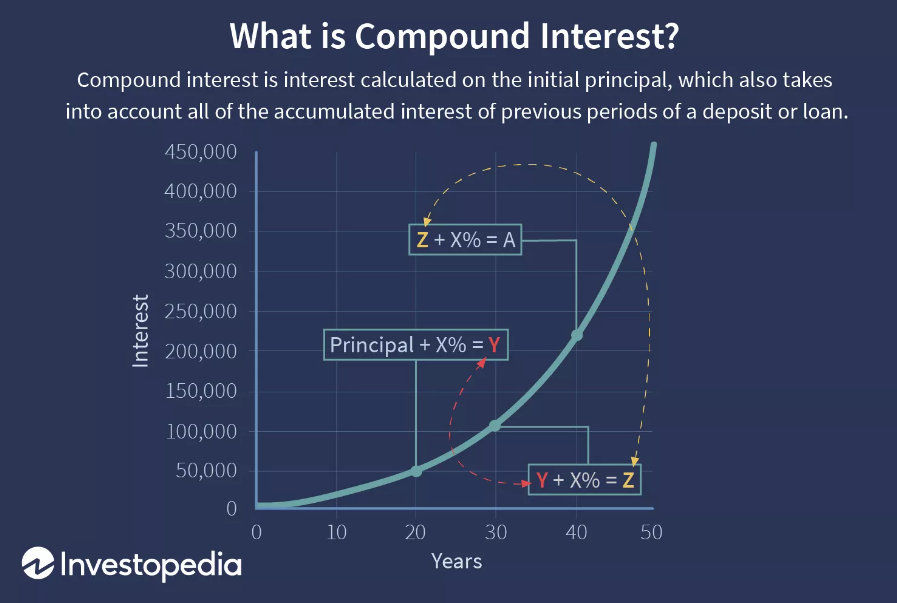

There are a variety of investments and investment vehicles to consider when balancing school, student debt, and other priorities. However, the principles of compounding interest, starting early, and time in the market > timing the market, will never change. Compound interest = interest calculated on both initial principal and all of the previously accumulated interest (interest on interest).4 As a result, the higher the number of compounding periods, the larger the effect of compounding. Over time, this amount increases exponentially, and starting early is the key. Even the smallest of contributions compounded over time will lead to large gains, assuming a set interest rate when accounted for inflation.

Types of investments vary, including cash and cash equivalents, T-bills, CD, stock market, money-market accounts, bonds, real estate, crypto currency, etc. A lot of these investments carry different amounts of risk, so always conduct your own due diligence before investing. However, many financial advisors recommend keeping it as simple and passive as you can, which involves buying/holding a low-cost exchange-traded fund (ETF) on the total stock market or S&P500 and focusing on pharmacy school. When it comes to certain retirement vehicles, there are two terms to consider: Roth vs. Traditional. Both of these types of accounts involve a tax-advantage, either when depositing or withdrawing money. A Roth account means that contributions are taxed, but the money grows tax-deferred and can be withdrawn tax-free after age 59.5. On the other hand, a Traditional retirement vehicle typically involves pre-tax contributions, but then the money grows tax-deferred with taxed withdrawals after age 59.5. Since students are in a lower tax bracket now vs. when they turn 59.5 years old, it is generally recommended to take advantage of Roth accounts as much as possible before significantly increasing your income, since you will be paying less money on the contributions.

Insurance

It’s a no-brainer that insurance to protect yourself, your family, and your assets is crucial. Many students remain on their parent’s health plans until the age of 26, but for those who don’t qualify or prefer to purchase their own insurance, below is a list of key policies to consider:

- Health insurance

- Consider a Health Savings Account with a lower premium but higher deductible to access another tax-advantaged investment account

- Auto insurance

- Can combine home and auto loan policies into one to obtain a lower rate

- Homeowners/renter’s insurance

- Hold pictures, spreadsheet, and receipts of all belongings that have value

- Umbrella policy

- Extra protection if own significant amount of assets and are at risk for being sued

- Life insurance

- Required if anyone relies on your income or if family would be in a tough spot

There are plenty of additional insurance policies to consider, but it all depends on your life situation and priorities. It’s generally recommended to consider a proper broker or financial advisor before making any insurance decisions.

Conclusion

Personal finance is truly personal, and there’s no one-size fits all approach to financial wellness. However, these key principles will assist any student beginning their journey to financial happiness with a rewarding lifestyle and peace of mind. Other resources regarding financial wellness, even as a resident, fellow, or practicing pharmacist, include:

- Books:

- Seven Figure Pharmacist - Tim Ulbrich & Tim Church

- Essentialism: The Disciplined Pursuit of Less - Greg McKeown

- Failing Forward - John Maxwell

- 7 Habits of Highly Effective People - Stephen Covey

- The 15 Invaluable Laws of Growth - John Maxwell

- The Miracle Morning - Hal Elrod

- The Compounding Effect - Darren Hardy

- The One Thing - Gary Keller & Jay Papasan

- Podcasts:

- Smart Passive Income

- Achieve Your Goals

- Entreleadership

- Your Financial Pharmacist

- Dave Ramsey

- The Money Guys

- Bigger Pockets

References

- https://www.aacp.org/sites/default/files/2023-08/2023-gss-national-summary-report.pdf

- https://www.investopedia.com/terms/p/personalfinance.asp

- https://www.nerdwallet.com/article/finance/best-budget-apps#personalcapital

- https://www.investopedia.com/terms/c/compoundinterest.asp

*Information presented on RxTeach does not represent the opinion of any specific company, organization, or team other than the authors themselves. No patient-provider relationship is created.